Before Roger Bannister first broke the 4-minute mile on the 6th May 1954, John Landy, an Australian runner, had run the mile in 4-minutes and two seconds on multiple occasions, but he described the barrier as a 'brick wall'. It took Bannister to break down that wall before Landy himself achieved the same milestone (when competing against Bannister at the 1954 Commonwealth Games). Bannister drew inspiration from the ascent of Mount Everest and early medical advancements (including an early Polio vaccine)... and he knew that barriers were more of a mindset than any hard limit. We discussed the race in an article titled "The Truth Behind The 100-Million Dollar Mortgage Broker" at a time before the pandemic, lower rates, and the apparent normalisation of triple-digit volumes, and the article focused on dismantling the arbitrary volume and growth targets many businesses impose upon themselves.

We're now just seeing a new breed of broker: the broker that is looking to achieve a billion in individual volume. What are they doing differently? In a sense, and from what we're able to resolve, these successful operations have simply detached themselves from the Groupthink collective and are instead forking off in new and creative ways, and they've discovered more effective ways of taming their dinosaur. Those businesses we work with that are seeing enormous success simply recognise that the model they're previously relied upon was a relic from the 1980s.

The industry is evolving in very positive ways, and this article seeks to identify why this is the case.

80 Knots: An SOP adhered to in most airliners and by most operators is the 80-knot call by the non-flying pilot. But what is the origin? Jay Beasley, author of "Patient Zero", and Lockheed test pilot, says the following: "Historically, piston engines at idle rpm while taxiing or holding for takeoff would foul the spark plugs causing uneven firing and roughness when takeoff power is applied. Usually they would start operating normally after a short period at high power. If they didn’t you aborted the takeoff. At Lockheed we concluded that we could stop a P-2 abeam the Fire House but any distance beyond was critical for aborts. At this time the airspeed was usually about 80 knots. This became a useful number which is now industry wide. Since it did become a number it was elected to adapt it to the P-3... "

The 80-call is now used in about every aircraft for a number of reasons, such as an airspeed check, pilot incapacitation, transition into the higher-speed phase, and so on. The point is that an arbitrary number - determined by the position of a fire hose abeam the runway - is now a standard call on virtually every commercial flight. A lot of what we do is inherited from obsolescence. Rather than remove an SOP, the industry simply reassigned its purpose. Now, the call is probably a bad example because the reassignment was done so for valid reasons.

Have you head the story about how the railway gauge was based on Roman Chariots? The story is reproduced below from an early version, and we've removed paragraphs:

Horses Arse: Here is a look into the corporate mind that is very interesting, educational, historical, completely true, and hysterical all at the same time: The US standard railroad gauge (width between the two rails) is 4 feet, 8.5 inches. That's an exceedingly odd number. Why was that gauge used? Because that's the way they built them in England, and the US railroads were built by English expatriates. Why did the English build them like that? Because the first rail lines were built by the same people who built the pre-railroad tramways, and that's the gauge they used. Why did "they" use that gauge then? Because the people who built the tramways used the same jigs and tools that they used for building wagons which used that wheel spacing. Okay! Why did the wagons have that particular odd wheel spacing? Well, if they tried to use any other spacing, the wagon wheels would break on some of the old, long distance roads in England, because that's the spacing of the wheel ruts. So who built those old rutted roads? The first long distance roads in Europe (and England) were built by Imperial Rome for their legions. The roads have been used ever since. And the ruts in the roads? Roman war chariots first formed the initial ruts, which everyone else had to match for fear of destroying their wagon wheels. Since the chariots were made for (or by) Imperial Rome, they were all alike in the matter of wheel spacing. The United States standard railroad gauge of 4 feet, 8.5 inches derives from the original specification for an Imperial Roman war chariot. Specifications and bureaucracies live forever. So the next time you are handed a specification and wonder what horse's ass came up with it, you may be exactly right, because the Imperial Roman war chariots were made just wide enough to accommodate the back ends of two war horses.

There's an interesting extension to the story about railroad gauges and horses' behinds:

Booster Rockets: When we see a Space Shuttle sitting on its launch pad, there are two big booster rockets attached to the sides of the main fuel tank. These are solid rocket boosters, or SRBs. The SRBs are made by Thiokol at their factory in Utah. The engineers who designed the SRBs might have preferred to make them a bit fatter, but the SRBs had to be shipped by train from the factory to the launch site. The railroad line from the factory had to run through a tunnel in the mountains. The SRBs had to fit through that tunnel. The tunnel is slightly wider than the railroad track, and the railroad track is about as wide as two horses' behinds. So, the major design feature of what is arguably the world's most advanced transportation system was determined over two thousand years ago by the width of a Horse's Ass!

While the factual nature of the stories are challenged, the adoption of new ideas based on inheriting deprecated machinery or ideas is entirely commonplace in industry, and it does indicate how antiquated 'anything' finds its place in the modern world.

From our Truth article, we wrote the following:

The notion that "extraordinary is the opposite of what everybody else is doing" isn't derived from what a business does, but also how it thinks. Impossible is a word to be found only in the dictionary of fools.

The only way to challenge any arbitrary man-made limit or fact is to break it. If it doesn't break, try harder.

In the last 12 months, and more than ever before, we're starting to see a bizarre style of survivorship bias, or a bias that applies when brokers look to emulate the behaviour and patterns of those brokers that they perceive are doing well, despite the fact those business behaviours and operating styles that are publicly discussed by the operators are also shared by those that are doing poorly. These businesses do a good job of keeping their 'secrets' closely guarded, so when these high-performers do speak to groups - usually at the behest of an aggregator - they'll often do so in a generic manner without exposing their proprietary methods, thus they'll often encourage others to emulate behaviours without communicating exactly what those behaviours are.

We've come in contact with businesses over the last year that are truly amazing, while others do business with operating ideologies that are bad - seriously bad (and they're highly reluctant to any guidance we might provide). As a company that thrives on innovation, dealing with a business that is shrouded in a Blockbuster mentality is seriously frustrating (this applies when we work with a business directly, and this close contact is now the exception rather than a rule). Dealing with some businesses reminds me of Eastern Airlines flight 401, the Lockheed Tristar. Crewed by three pilots with one dead-heading pilot, Flight 401 was so consumed with changing a light bulb that they simply forgot to fly the aircraft, and ultimately crashed in the Florida Everglades. Then there's Air France 447; in 2009 the aircraft was operating from Rio to Paris and plunged into the Atlantic after some preventable icing problems. The list goes on and on. In aviation - despite the regimented approach to safety, and a discipline that is found in no other industry - pilots ignore the warning signs and crash... and I see the same happen in the mortgage industry all the time.

A group of scientists placed fleas into a jar. They jumped out. The same scientists placed a lid on the jar for a few days and then took the lid off and observed that the fleas had adapted to their new norm. For the rest of their lives, the fleas only jumped as high as the lid and never jumped any higher. Once the fleas reproduced, their offspring shared the same limitation. While there are troubling comparisons to our own lives and limitations, we see the brokers as living in what was once a sealed jar. The lid, once removed, was an absolute arbitrary limitation.

While we could simply brand the industry as 'resistant to change', which is true, the bigger problem is that we're committed to a model we know works (despite the fact it doesn't work very well).

Organisation Immune Systems is a concept of organisations having ‘Idea Antibodies’. The short version of a long story that involves a mashup of individual and business bias' is that an organisation will have an 'immune system' that protects 'the body' from damaging external influence... even when that external influence is a good idea. The 'damaging external influences' is an aggregated bias introduced by inexperience, fear, poor management, micromanagement, lack of processes and SOPs, and so on. When we're exposed to new ideas that challenge our own antiquated and objectively flawed understanding - despite the fact what you're exposed to will potentially introduce phenomenal success to your operation - the opportunity will often be dismissed because the business isn't mature or agile enough to understanding, let alone introduce, new programs or methodology. We've seen some businesses say that they "can't handle the volume", or "can't grow that quickly", despite the fact their existing operations are a blocked sewer that requires some serious work.

From an article on SOPs we wrote the following::

The bias' (as mentioned above) were introduced on the back of Rear Admiral Grace Murray Hopper's 'backwards clock. Hopper, an accomplished Naval officer, is often best remembered for her “We've always done it this way” quote:

As a Naval officer it’s likely that Hopper’s quote was motivated in part by the frustrations of working within a military bureaucracy resistant to any change. But as a programmer and Naval strategist she understood that information wasn’t of use unless it was shared, turned into intelligence or knowledge, and then further developed from best practice into better practice.

In the same article we wrote the following:

Organisations will often have immune systems and idea antibodies - it's the survival mechanism of fools fleas.

A personal or organisational confirmation bias is a dangerous thing. Confirmation bias is an inherent and stubborn flaw in the human condition. We like to validate our decisions and actions without a broader consideration outside the diagnosis that we initially form early on… and we’re inherently biased and emotionally motivated to form a hypothesis to support an original conclusion. We sometimes become completely invested in a decision and consumed with whatever action is required to confirm our original opinion (aggravated by the fact that we don’t have spare brain capacity to question what we’re doing). The psycho-babble suggests that our confidence systematically exceeds accuracy; implying we are often ‘more sure’ about something than we should be.

A confirmation bias will often lead to a Commitment Bias born from overconfidence. Overconfidence leads to a situation where we form an irrational escalation of commitment, or commitment bias, leading to anchoring (or tunnel vision). The longer we vacate dynamic lateral thinking and tolerate a cognitive dissonance, the more and more we commit to a bad decision and “make the wrong decision the right decision”. So, the whole “we’ve always done it this way” quote slowly takes on another form; "I have to do it this way because this is what works".

Sadly, these inward bias' born from a binary style of business management leads to the dreaded Dunning-Kruger bias. In the field of psychology, the Dunning–Kruger effect is a cognitive bias in which people of low ability have illusory superiority and mistakenly assess their cognitive ability as greater than it is. The cognitive bias of illusory superiority comes from the inability of low-ability (of high confidence) people to recognise their lack of ability. Without the self-awareness of metacognition, low-ability people cannot objectively evaluate their actual competence or incompetence. Most brokers have their own business, and they all like to think they're 'better than the other guy' despite no objectivity supporting their claim. The most common Kruger style of management comes from small businesses with small teams where the director of the operation carries the burden of that dreaded Blockbuster mindset (meaning you're fixed to obsolete methods).

The mortgage industry is made up of a mishmash of personalities, often drawn to the profession by way of necessity or the low barrier to entry. What happens when you attract people from defunct or dying industries, or those that previously and very casually walked a business tight-rope into shark-infested waters? The experience creates a hard limit. It's this emotionally-cautious group where we see most businesses apply a debilitating caution... and it's where we've mistakenly invested some of our own time in the past. Homer Simpson once said that "you tried your best and you failed miserably. The lesson is, never try"... and we can't help but feel some brokers have a mindset that was altered by their previous failed environment, so they'll adopt a 'safe' management style that that is structured in such a way that it can't or won't scale.

Aggregation: Aggregation is part of the problem... but they're also a big part of the solution. During the BRC I participated in a focus group that looked at the role of aggregation, and this was at a time when brokers were unfairly criticised for their commission structure, but very few questioned the funds paid to aggregators. AFG, for example, has nearly 300 staff, meaning that just the rationalised salaries and benefits paid out to employees every week hovers close to a million dollars. At the time of the BRC, the facilities for brokers to operate autonomously didn't exist, but we're closer to that now than we were in the past, particularly with the demonstrated adoption of standards applied to Open Banking. Aggregation are an organisational group that is extremely reluctant to alter their model because what they have works. Aggregators rightfully subscribe to the notion that if system artifacts are stable and do not threaten the future of the legacy system, and these systems are not 'broken', or they do not threaten the business structure, then the existing operating ideology shouldn't be altered. However, this isn't the role of aggregation. If aggregation continues to be required, shouldn't they introduce new, dynamic, and out-of-the-box projects to their brokers? AFG, Finsure, and others, still provide what can only be described as the worst website experiences in the industry, but changing their position - despite the massive advantages that change would introduce - is impossible. Aggregators are not an agile operation in any respect. Your business will usually survive in spite of aggregation, not because of it. The question aggregators need to ask themselves is simple: would a broker continue working with us if they didn't have to?

We appreciate that our concepts are sometimes unconventional. Our digital solutions are different (because they have to be), and our relationship programs are usually lost on those that celebrate mediocrity. However, they just work. If you're doing what everybody else is doing, you can only expect the same mediocre results.

We believe that no broker should even lower themselves to a point where they'll purchase leads (usually non-compliant acquisition), and we usually discourage brokers from seeking a 'generic' coach (there are genuinely coaches in the industry that advertise 70m in yearly volume... yet we see that volume routinely from some businesses every month).

If you don't have digital integrated into your business, or you don't have the immediate capacity to generate leads or promote products right now, you're literally living in a finance stone-age, and you need to call us.

We're a fintech company, so our services are orientated around digital, and we rarely consult these days as a result of an increasing workload. Our mortgage broker website framework is just one tool we provide out of necessary, and it will obviously improve your digital success, and those lead generation programs we provide far exceed the ROI returned via the dodgy lead-generation crowd, but it is those programs we provide brokers on the periphery will have a ridiculously positive impact on your operation. However, despite providing solutions, we still encounter those that 'just don't get it', or they're so consumed with a personal or organisational bias that they'll continue to casually stroll further and deeper it a realm defined by worst-practice. As part of standard support we try and unplug brokers from the matrix and introduce them to the real world, but we can only provide the tools.

This article is in no way criticism of the industry. I continue to have enormous respect for the work brokers do, and to that end, I'd like to see those businesses that operate a slick ship attract more growth. I see brokerages with 5 staff writing around 100-million a year and it genuinely keeps me up at night.

What are you doing this year to challenge your understanding of the architecture that underpins your operation? What programs are you introducing to improve customer service and attract more high quality business? How are you going to amplify the effectiveness of your partner program? What digital measure are you putting in place to automate your pipeline and processing?

We'd suggest you think out of the box, but in this case it seems more appropriate to think out of the jar. Want to lift the lid on some of the programs some of the most successful operations in the country are using to build their business? Call us to learn more.

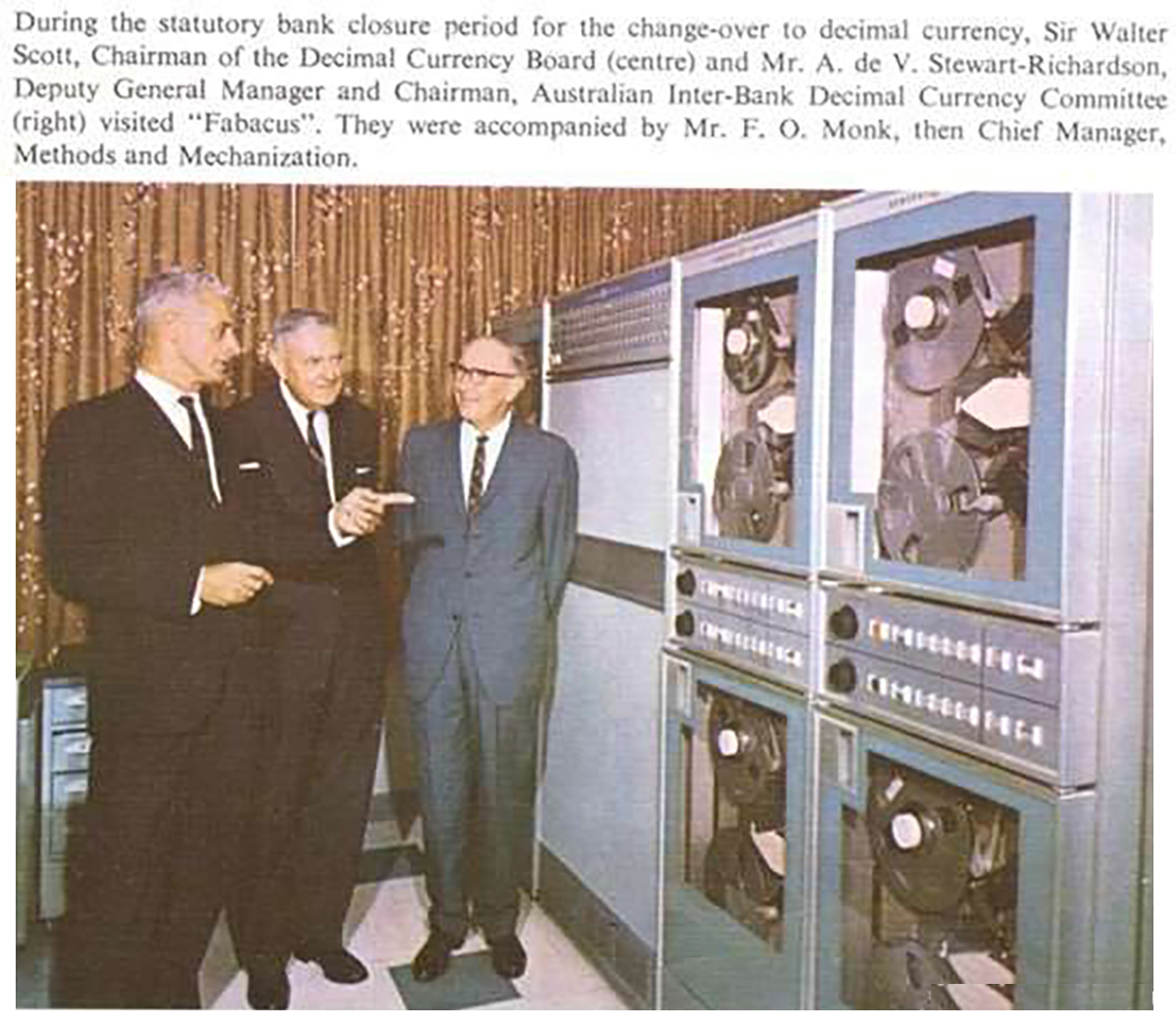

in Sydney saw the bank expand its operations to all interstate branches, and it later built additional computer centres in Melbourne, Brisbane and Perth. The team that worked on the computer were dealing with new technology and had no guidelines to follow - nor did they have any experience with technology. The IT roles were generally assigned to women and computing was still considered a suitable processing role (image shows two of the first three women operators of the computer: Gayle Carwardine and Eileen Chalmers. Source: Westpac). The GE computer was eventually phased out after the bank opted to go with IBM in 1970. FABACUS was replaced by a Honeywell H-060, which ran the GE’s programs under simulation, so the bank had breathing room to convert all its systems to IBM protocols.Text provided by Westpac. In the case of computers, it took Westpac to innovate before others followed, and they did so with an agility that was entirely uncommon to the era; however, they recognised the need for innovation. Read about the day "Westpac turned Internet banking on

in Sydney saw the bank expand its operations to all interstate branches, and it later built additional computer centres in Melbourne, Brisbane and Perth. The team that worked on the computer were dealing with new technology and had no guidelines to follow - nor did they have any experience with technology. The IT roles were generally assigned to women and computing was still considered a suitable processing role (image shows two of the first three women operators of the computer: Gayle Carwardine and Eileen Chalmers. Source: Westpac). The GE computer was eventually phased out after the bank opted to go with IBM in 1970. FABACUS was replaced by a Honeywell H-060, which ran the GE’s programs under simulation, so the bank had breathing room to convert all its systems to IBM protocols.Text provided by Westpac. In the case of computers, it took Westpac to innovate before others followed, and they did so with an agility that was entirely uncommon to the era; however, they recognised the need for innovation. Read about the day "Westpac turned Internet banking on  ", another example of Westpac altering the status quo through forward-thinking innovation.

", another example of Westpac altering the status quo through forward-thinking innovation. Pictured is a General Electric 225 computer System. In the foreground is a table with a reel of magnetic tape on top. In the background is the system with console on the left, with a plotter and typewriter on console table. Behind the console are the system cabinets with two magnetic tape drives to their right. [ View Image ]

{kind=link}

{kind=link}

{kind=link}